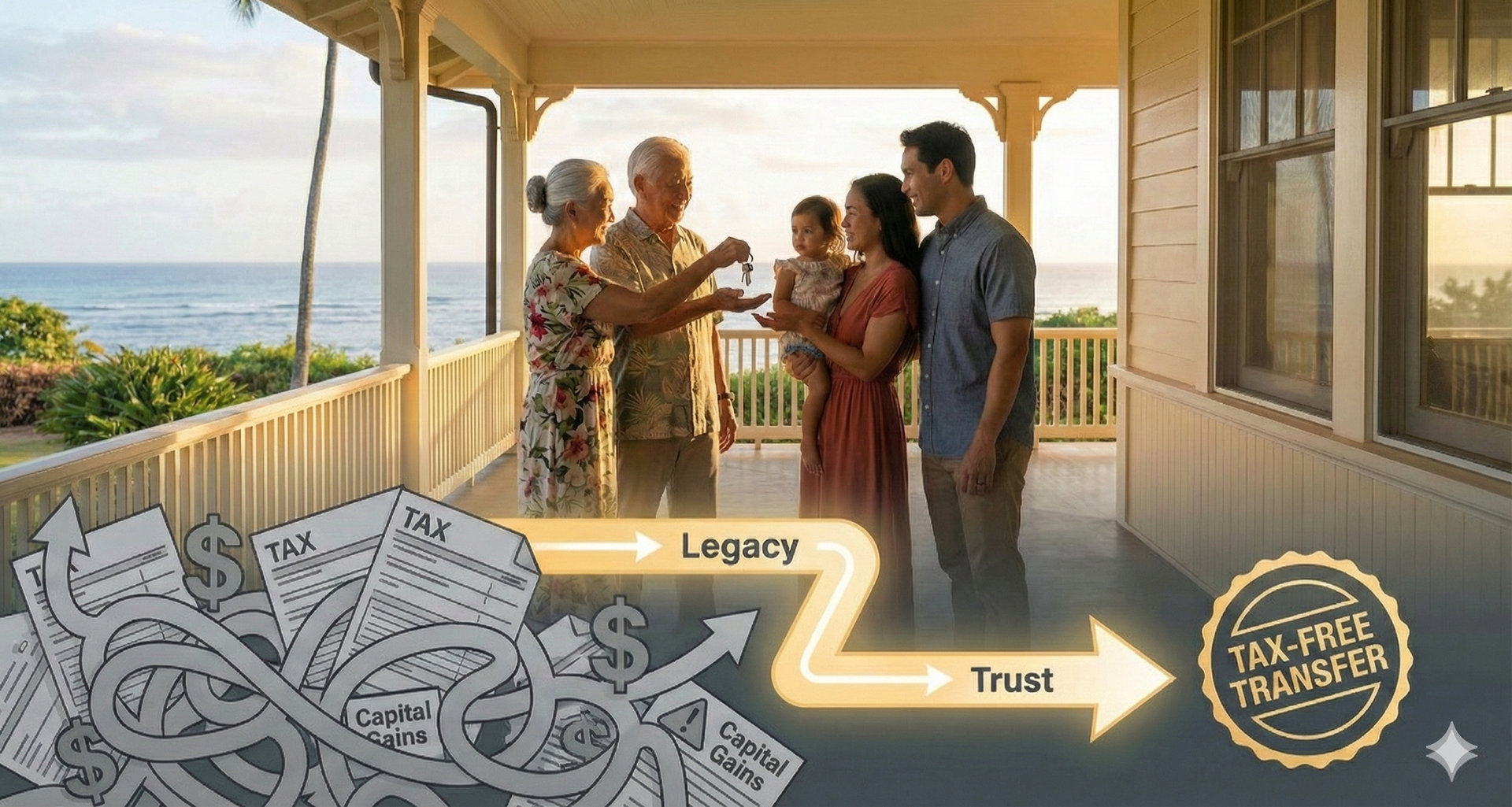

Gifting vs. Inheriting: What is the Best Way to Pass Down a Hawaii Home?

One trend I see constantly here in Oahu is the deep desire families have to preserve their legacy. It is a beautiful sentiment. But here is the hard truth that many families don't realize until it's too late: How a home is passed down determines whether it becomes a financial blessing or a massive tax burden.

Families often imagine the home will stay in the family forever, but it’s best to avoid a scenario where heirs feel "trapped" and afraid to sell because they would lose a third of the value to taxes. To ensure this remains the "Ultimate Gift," families must navigate the "Tax Matrix" correctly. Here is a simple guide to keeping the legacy in the family and out of the hands of the IRS.

The Big Trap: The "Lifetime Gift" Mistake

The biggest financial threat to a family legacy is Capital Gains Tax, and it usually happens when parents try to do something nice: giving the house to the kids while they are still alive. Consider this typical Honolulu scenario: Parents bought a home in 1980 for $100,000. Today, that same home is likely worth $1.2 million. That is $1.1 million in growth. If parents transfer the title now (or add their children to the deed), the children legally inherit that original $100,000 purchase price as their "tax basis." They don't just get the house; they get the looming tax bill, too. If the children ever need to sell the home later for $1.2M, the IRS will tax them on the full $1.1M of growth. Between Federal and Hawaii taxes, that could wipe out 30% of their profit—a $300,000 mistake that could have been avoided.

The "Inheritance" Strategy (The Magic of the Step-Up)

The tax code favors waiting. If the title passes only after the parents pass away, the value of the home gets a "Step-Up in Basis."

- What this means: The IRS hits a reset button. They treat the home’s value as if the heirs bought it on the day the parents passed ($1.2M).

- The Result: If the heirs sell it immediately for $1.2M, their taxable gain is zero. The family just saved hundreds of thousands of dollars.

So, How Should Families Transfer the Title?

There are four main options to pass down a home in Hawaii. Here is how they stack up, from best to worst.

1. The Revocable Living Trust (The Gold Standard)

Most experts agree this is the best way to transfer Hawaii real estate.

- How it works: The parents change the title from their individual names to "Trustees of the Family Trust."

- The Pros: It avoids Probate entirely (saving the family months of court time and 3-5% in fees). It also protects the "Step-Up" tax benefit mentioned above.

- The Cons: It costs a little money upfront to set up.

2. The Transfer on Death Deed (The "Easy Button")

Hawaii allows a special deed (TODD) where homeowners designate a beneficiary, but the transfer doesn't happen until death.

- The Pros: It’s cheap, simple, and parents keep full control of the house while alive. It also protects the "Step-Up" tax benefit.

- The Cons: The law gives creditors up to 18 months after the owner’s death to file claims against the property. This often leaves title insurance companies unable to insure these homes during that period. Without title insurance, selling is difficult. In this scenario, heirs would likely have to wait 18 months to sell.

3. Joint Tenancy with Rights of Survivorship (The "DIY" Method)

This is the common "do-it-yourself" strategy where parents simply add a child to the deed. It seems easy, but families should proceed with caution—there are hidden traps.

- The Paperwork (Gift Tax): Parents must legally file Form 709 to report the transfer. While they likely won't owe actual taxes immediately (unless they have exceeded the $13M lifetime exemption), it is mandatory federal paperwork.

- The "Step-Up" Loss: This is the big financial hit. By gifting a share of the house now, the child inherits the original (low) purchase price on that share. The family loses the massive tax-free "step-up" benefit for the portion given away.

- Liability Risk: Once a child is on the deed, the house becomes their asset, too. If the child gets divorced, files for bankruptcy, or is sued, the parents' home could be at risk to settle those debts.

- The Medicaid Trap: This is a critical point many forget. If a parent ever needs to apply for Medicaid long-term care, the government looks back at financials for the last 5 years. Giving away a share of the home counts as a "disqualifying gift," which could cause coverage to be denied.

- Property Tax Issues: If the child doesn’t live in the home, the property may lose existing homeowner exemptions, causing property taxes to increase.

4. The Last Will and Testament (The Slow Lane)

If the house is simply left in a Will, the family is guaranteed a trip to court.

- The Risk: Wills must go through Probate. The home could be "stuck" in the legal system for 1–2 years, preventing the family from selling or refinancing when they might need to most.

- Pros: It is generally less expensive upfront than creating a Trust.

"A-PEELE-ING" Tip!

What if parents want to transfer their home early, without waiting until they pass away, but still hope to avoid significant capital gains?

Sell the Home to the Next Generation (The Creative Solution)

- How it works: Parents sell the home to their children at fair market value using an Installment Sale. Since the gain is spread over many years, the parents receive income without triggering the full capital gain all at once. This strategy often keeps them in a lower tax bracket, allowing them to avoid paying a substantial amount in capital gains.

- The Benefit: The heirs pay the parents over time (mom and dad become the bank). The parents get cash flow, and the kids get ownership without waiting for a death in the family!

Crazier idea: The parents can even rent the property back from their kids if they wish to stay in the home. This is called a Leaseback, and it opens up tax deductions for the children (now the owners). This is a surprisingly elegant solution for families who want to keep the home "in the family."

A Note on Hawaii Taxes

Living in paradise comes with its own rules.

- Estate Tax: Hawaii has a lower threshold than the Feds. If the total estate is over $5.49 million, the state wants a cut (10–20%).

- Conveyance Tax: Every time a title moves, Hawaii charges a fee. However, if done correctly (like transferring to a Trust or a child for "nominal consideration"), families can claim exemptions (Exemption 4 or 9 on Form P-64B) to avoid this.

The Bottom Line

A home is likely a family's biggest asset. "Gifting" it isn't just about handing over the keys; it's about handing over a clean title and a smart tax strategy. Whether you want to explore the Installment Sale strategy or just ensure your Trust is set up correctly for Oahu's specific market, you don't have to figure it out alone. I can help you value your property and connect you with the right tax professionals to build a plan that works for your ohana. Contact me today for a complimentary home valuation.

Disclaimer: I am a real estate expert, not a CPA or Attorney. This is for information only—always verify your strategy with a qualified tax professional!